This week in ‘Expert Speaks’ section we have Mr. Prashant Jain, Executive Director and CIO of HDFC Mutual Fund. He is the most consistent fund manager for the last two decades. It’s a fantastic piece and I am sure one will find lot of take away from this note.

‘In good time every one invests, in adverse time does none,

To the wise one who invests in bad times ,wealth should come.

Its tomorrow that matters

Good returns are seldom made on investments made in good times. Rather, good returns are typically made on investments made in adverse times. There is a fair value for listed companies, just like for companies that are not listed. In good times when the stock markets are doing well, companies typically trade above fair values and in adverse times when markets are not doing well they tend to trade below fair values. In the long run, markets do not sustain at either overvalued or undervalued levels, rather move close to fair values. This is why investments made in adverse times typically yield above average returns and vice versa.

The tables below clearly bear this out. (Source: Bloomberg)

This table summarises the 3 and 5 year returns for the Sensex from times when the environment was good, market sentiment was positive and valuations were expensive, post year 2000.

Table A: Performance of investments made in good times

| Time | Sensex Level | 1 year forward P/E | Main news / reasons | Total Returns after 3 years# | Total Returns after 5 years# |

|---|---|---|---|---|---|

| Jan-00 | 5205 | 25 | High optimism in technology stocks | -38% | 26% |

| Dec-07 | 20287 | 26 | Booming global economy, optimistic markets | 1% | -15% |

This table summarises the 3 and 5 year returns for the Sensex from times when the environment was challenging, market sentiment was negative and valuations were low, post year 2000.

| Time** | Sensex Level | 1 year forward P/E | Main news / reasons | Total Returns after 3 years# | Total Returns after 5 years# |

|---|---|---|---|---|---|

| Oct-01 | 2989 | 11 | 9/11 attack on WTC, global markets collapse | 91% | 334% |

| June-04 | 4795 | 10 | Unexpected defeat of BJP in general elections | 61% | 99% |

| Nov-08 | 9093 | 11 | Sub-prime crisis - Lehman collapse | 77% | N.A. |

From the above it is clear that markets do not sustain at either overvalued (high P/E) or undervalued (low P/E) levels and revert close to fair levels over time.

Besides, the fair value of markets / companies is not stagnant; rather it is increasing at

- # Dividends not accounted for ; Past Performance of the Sensex may or may not be sustained in future.

- ** Index level is taken as on the next month end after the crisis; * This return is from Dec 2007 till April 2012

- The above tables are for illustration purposes only and should not be construed as an investment advice. It does not in any manner imply or suggest current or future performance of any HDFC Mutual Fund Scheme(s).

roughly 15% p.a. This rate is broadly the same as the nominal growth rate of GDP since companies in aggregate represent the economy itself. India’s nominal GDP growth rate (real growth rate plus inflation) has been 14.1% p.a. since 1979. Current GDP growth rates over last 3 years of 16% p.a. (7.9% p.a. real growth and 8.1% p.a. inflation) are similar. It is not surprising therefore, that the Sensex has yielded nearly 15% p.a. returns from inception in 1979 till date # .

Collective expertise at mistiming

Buy low and sell high is what everyone suggests and that is what everyone would like to do.

The reality however for a typical investor in equity markets / equity mutual funds is somewhat like this – buy high, buy more higher, buy even more even higher, buy less when market falls, buy lesser if markets fall more and buy nothing when markets are really down.

This behavior is best illustrated by the following table.

Table C: Annual net sales of equity funds across different phases of the market

(Source: Equity net sales – AMFI ; Average forward P/E is the monthly average P/E for the year – Bloomberg)

It is quite evident from the above that as the Sensex went up from 3000 levels in 2003 to a peak of above 21000 in January 2008 before ending close to 15600 levels in March 2008 net sales of equity mutual funds increased from just Rs 118 crs in FY03 to Rs 53,000 crs in FY08. Since then, in down markets and at lower P/E multiples over the

#

At 16.6% CAGR over 1979 - 2012, 100 has become 16000 (160 times). This is the magic of compounding and that’s why it is said that time in the markets is more important than timing the markets.

last 4 years (FY 09 – FY12) cumulative flows into equity funds have been a negative Rs. (-) 6000 crs. In simple terms, when P/Es were high, more than Rs 50,000 crs worth of equity funds were purchased in one year in FY08 and when P/E s were lower, nearly Rs 6000 crs worth of equity funds were sold / redeemed by investors between FY09 – FY12.

More specifically, between October 2007 and March 2008, when the Sensex was near 20,000 levels, the net sales of equity mutual funds were Rs. 41,142 crs. On the other hand, just a year later, between October 2008 and March 09 when the Sensex was below 10,000, sales of equity funds were a negative Rs. 162 crs.

This was not the first time that such a thing happened. Between 1988 and 1992, after the Sensex had gone up a staggering 10 times from 400 levels to 4000 levels and the P/E’s had reached an all time high of 40 times, a Mutual Fund equity scheme collected nearly 4000 crs (at today’s prices this should be more than Rs 20,000 crs); similarly during the IT boom, billions were invested in IT, not to forget a similar trend in real estate and in related sectors in 2007.

This pattern of an overwhelming majority of investors mistiming the markets repeatedly and consistently is a key reason for the unsatisfactory experience of the majority from equities and for the poor equities ownership in India.

While there can be many reasons for this collective expertise at mistiming, the key reason probably is:

A majority of investments in equities are not done with a long term view, despite the fact that the best that equities have to offer is only over long periods. This is unfortunate, as by investing with a short term view, investors are not benefiting from the compounding potential of equities.

Einstein once remarked “Compound interest is the eighth wonder of the world”.

At 15% CAGR, 1 becomes nearly

2 in 5 years

5 in 11 years

10 in 17 years

20 in 22 years

confidence and greed both keep on increasing, leading to even larger inflows. Similarly, in downward moving markets, the expectation is that the markets will keep on moving lower, leading to lower inflows; the lower the markets move, or the longer the markets do not move, higher is the confidence, that markets will fall further or that markets are going nowhere, resulting in drying up of fresh investments or even redemption of existing investments.

Also, when markets are moving up, the news flow is generally good and vice versa. Therefore, generally, in rising markets the perceived risk is low whereas the actual risk is higher as valuations are high. On the other hand, in adverse times, when the markets are not doing well and the news flow is not good, the perceived risk is high whereas the actual risk is lower as valuations are attractive.

The net result of all this is, that time and again, a majority of investors end up investing large amounts at high valuations and small amounts at low valuations. Clearly, such an approach to investments is not conducive to generating good returns and if followed, is likely to lead to disappointing results time and again.

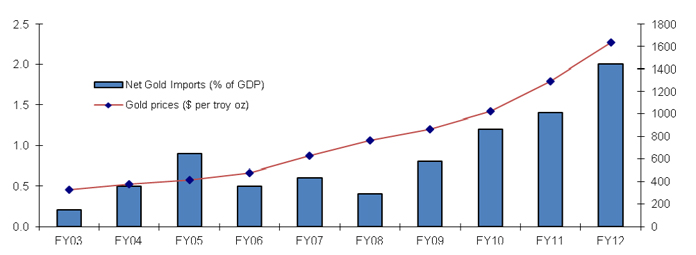

A very similar behaviour of investing increasing amounts as prices go up has been observed in gold over last several years (refer chart below).

Chart 1 – Net gold imports (% to GDP) and average annual gold prices

As gold prices kept on rising every single year for the last many years (they are up nearly 6 times in 10 years), annual investments in gold by Indians have gone from $ 0.9 bn (0.2 % of GDP, 0.7% of Household savings) in FY2003 to ~ $ 36 bn (~2 % of GDP, ~10% of Household savings) in FY12 (Source: Citi Research estimates).

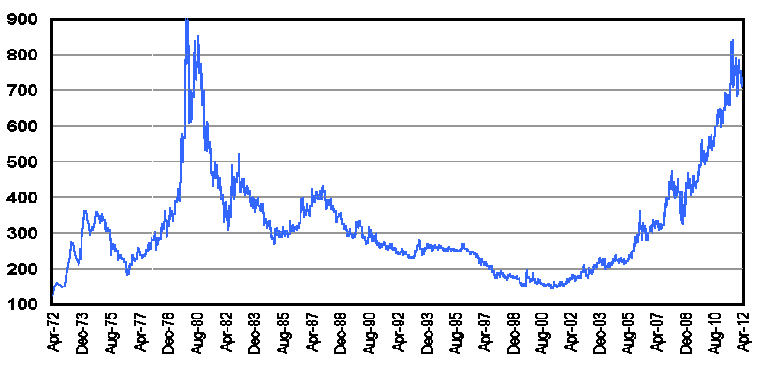

If similar past experiences of a rapid rise in the price of an asset class accompanied by a dramatic increase in investments in that asset are anything to go by, then, these vast sums invested in gold, particularly over last few years, may not meet expectations. The chart below that gives the real prices of Gold in USD terms is very illustrative and also suggests a similar conclusion. The last time Gold prices were at current levels in real terms was in January 1980, a good 32 years earlier.

Chart 2 – Gold prices adjusted for US inflation in USD

(Source: Bloomberg)

In other words, Gold prices in real terms are presently once again at a level from where they have yielded nil real returns after 32 long years.

From Table C and Chart 1 it is clear that there is a striking similarity in the investment patterns of millions of individuals for two very different assets like gold and equities. This is probably because even though the asset classes are different, the individuals involved and their thought processes are the same. A majority of investors simply chase returns and tend to invest increasing amounts as prices continue to rise on one hand and tend to reduce investments when the prices fall or do not rise for long periods on the other.

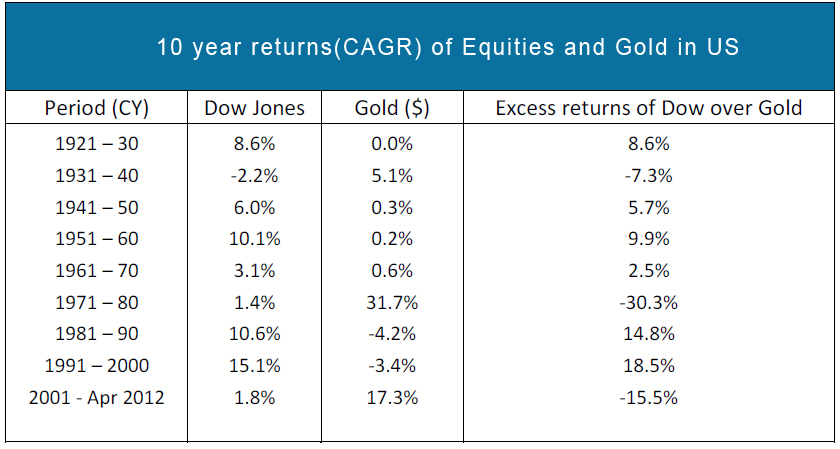

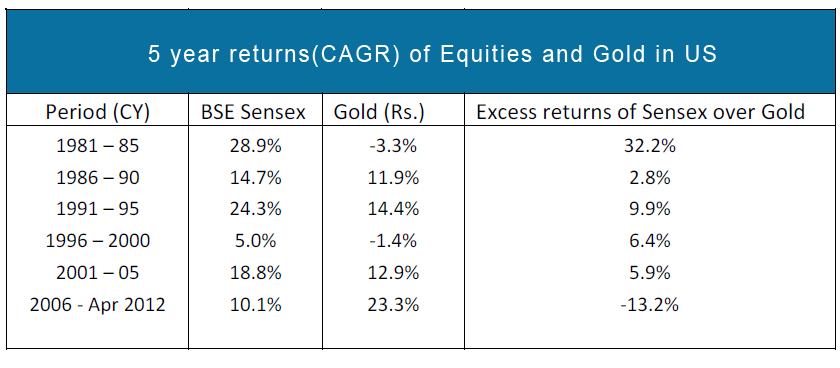

Such an approach to investments is clearly not returns friendly and it therefore comes as no surprise that a majority of investors probably do not get rich by investing. Faced with unsatisfactory returns, most blame the markets when instead, it is the investment approach that is flawed and that needs to be corrected. However, in case of gold, Indians are forgiving as few compute CAGR or IRR and as the time horizons are very long, often bordering on indefinite, even though gold has underperformed equities in a majority of 5 / 10 year periods. (Refer Table D on next page)

Table D: Returns of Equities and Gold in US and in India

(Source: Bloomberg, estimates)

Past performance may or may not be sustained in future

It must be highlighted that there were and there continue to be very divergent views on Gold. The above comments on Gold should be taken more as observations and not as a wellresearched or comprehensive view on Gold.

Key challenges facing the Indian economy

It is true that the economy is currently passing through a difficult phase. However, this is neither the first nor will it be the last time the economy is facing challenges. Besides, the problems facing the economy are such that should get resolved over time and through some specific steps.

The following is a summary of the key concerns that the economy / stock markets are faced with:

High Fiscal deficit: This has been the key concern in India over the last few years. Fortunately at one level and unfortunately at another, this is an issue that is of our own making and therefore the solution is in our reach too. Though some steps have been taken in the last budget, the real solution lies in eliminating / sharply reducing the diesel subsidies. Despite several disappointments on this front over last several years, there is hope that this will be tackled on a priority basis as the dangers of not tackling this are hidden from none.

High Current account deficit (CAD): The worsening of current account deficit over last few years from 1.3% of GDP in FY08 to nearly 3.8% in FY12 (market estimates) is almost entirely on account of increase in gold imports from 0.4% of GDP in FY08 to 2.3% (E) of GDP in FY12. Looking at the sharp rally in gold prices over last several years, investor behaviour that is so typical of such situations, significant moderation in USD gold prices over last year and sharp moderation in recent gold import volumes, it appears that the highest gold imports are behind us. If this is indeed the case, then as and when gold imports revert closer to longer-term average of 0.5% of GDP, the CAD should get addressed progressively in the current and over the next few years. The sharp INR depreciation should also moderate CAD in FY13 and beyond by making exports more competitive and imports costlier.

Depreciating INR: This is a result of high CAD and of poor investment sentiment leading to weak capital flows. Though forecasting currencies is harder than stock markets, it has been experienced that when there is a consensus in one direction, that is where the turning point often is. A nearly 25% depreciation in less than one year of the currency of a large economy like India is not a small movement and it appears to be excessive. What could also come to the help of the INR is the expected improvement in CAD in FY13, any policy steps that improve investment sentiment, notably reducing fuel subsidies and / or any moderation in global crude oil prices.

European Crisis: Though the way forward of European crisis is hard to figure out, most would agree that the impact of the European crisis on the Indian economy and therefore on the equity markets over long periods should be much less than on other countries. This is so because India’s exports / investments in the stressed economies of Europe are miniscule.

Between April 2010 (when Greek Government debt was downgraded to junk status) and now, other than the markets of countries that are stressed, Indian markets are one of the worst performing globally across both developed and emerging markets. This indicates that the Indian markets are probably impacted more by India specific issues and not by the European crisis. It is interesting to note that DAX (German stock market index) is marginally up in this period whereas India is down 10%.

GAAR : This appears to have been commented upon sufficiently to assume that this has been discounted by the markets.

In the face of so many issues and adverse news flow almost on a daily basis, it is easy to forget the several strengths of the Indian economy. These are large availability of natural resources other than oil, favourable demographics, rising incomes, high household savings rate, low penetration of consumer durables, rising competitiveness of exports due to sharp depreciation of INR (particularly vs Yuan), slowly but steadily improving infrastructure, etc. Though these strengths seldom make headlines, they are intact and should lead to continued economic growth in future as they have in the past.

Global crude prices are correcting rapidly. OPEC and Saudi officials have openly remarked that they are comfortable with Brent Crude at $100. Negotiations with Iran on nuclear sanctions are also reportedly progressing. If oil prices stabilize at lower levels, pressure on fiscal / current account deficits and INR will quickly ease. Lower interest rates will then be a natural outcome and will support a much-needed revival in Capex.

The current problems facing the economy are not insurmountable. The solution lies in a few difficult decisions. As difficult changes typically take place in difficult situations when there are no easier options left, it is hoped that we will not have to wait for long. With few such steps and over time, it should be possible to put the economy back on the rails fairly quickly.

Difficult markets or bargain markets?

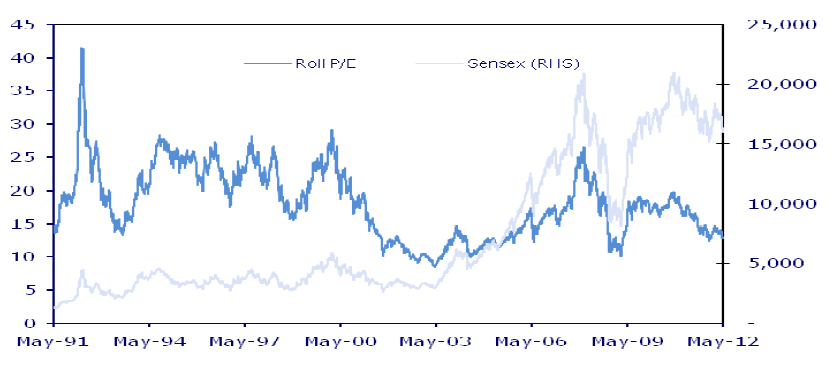

The stock markets are passing through a difficult phase. The values of the listed businesses as indicated by the Sensex are down by 20% between 2008 – 2012 (presently SENSEX level is 16000 compared to 21000 seen in early 2008). This is despite a nearly 60% growth in the GDP (15% CAGR) and therefore a similar growth in the fair values of businesses over the same time. Consequently, one year forward P/E multiples have come down sharply from over 20 times in FY08 to below 13 times presently. These are nearly 20% below the long term averages. Further, the P/E of the Sensex based on FY14 (E) EPS of 1475

(source : BOFA ML) is nearly 11 times, which is close to the lowest multiples that Indian markets have traded at in the past.

Chart 3 – 1 year forward P/E of the Sensex (Source: CLSA)

Bargains are available only in challenging environments / in markets characterized by weak sentiment and seldom when the going is good / sentiment is strong. That’s why, from an investor’s perspective, a more appropriate way to describe the current markets would be bargain markets and not difficult markets.

God and Equities

This is a couplet by Saint Kabir, a much loved and revered saint of 15th century who lived near Varanasi – which many believe is the oldest city in the world to have survived continuously.

This couplet reads as follows:

Dukh Mein Sumiran Sab Kare, Sukh Mein Kare Na Koye

Jo Sukh Mein Sumiran Kare, Toh Dukh Kahe Ko Hoye

It means the following:

[ In anguish everyone prays to Him, in joy does none

To One who prays in happiness, how sorrow can come ]

Stock markets and God do not have much in common. Probably, that’s why, the above does apply to stock markets but in reverse.

An adapted version of the above for stock markets would be as follows:

[ In good times everyone invests, in adverse times does none

To the wise one who invests in bad times, wealth should come ]

The moral of this is that remember God in good times and equities in bad times. If this is done, then chances are one will avoid both - bad times in life and poor returns on investments.

Its tomorrow that matters

By the end of June or shortly thereafter, Greece will either be in Eurozone or it will not be. Over the same timeframe, steps if any, that are undertaken by the government to resolve some of the issues facing the economy will also be known. Irrespective of what happens, markets should discount these outcomes fairly quickly.

It is true that the economy is currently battling twin deficits, but that is known to the markets. What will determine markets of tomorrow, are the deficits of tomorrow and expectations thereof, both of which chances are will be better and not worse than today.

Times such as present, when the markets are not doing well should actually be looked upon as a window of opportunity for savers to invest more into equities, so that when the good times come, there are meaningful investments in equities to reap the benefits from. The lower the markets are, the bigger is the opportunity and the longer the markets remain depressed, better is the opportunity for savers. In a lifespan of investing of say 30-40 years, it is unlikely that the markets will provide many such windows. In the last 20 years there have been only 3-4 such windows.

Finally, what has taken several pages, Sir John Templeton conveyed more effectively in one line:

“Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

Needless to say, pessimism is all that one sees all around.

Prashant Jain

May 2012

P.S: Equities are a volatile asset class and only long-term surpluses should be invested in equities depending on an individual’s risk taking capacity; phasing out of investments over time reduces risk.

DISCLAIMER: The views expressed by Mr. Prashant Jain, Executive Director & Chief Investment Officer of HDFC Asset Management Company Limited, constitute his views as of May 24, 2012. The views are based on internal data, publicly available information and other sources believed to be reliable. Any calculations made are approximations, meant as guidelines only, which you must confirm before relying on them. The information contained in this document is for general purposes only. The document is given in summary form and does not purport to be complete.

The document does not have regard to specific investment objectives, financial situation and the particular needs of any specific person who may receive this document. The information/ data herein alone are not sufficient and should not be used for the development or implementation of an investment strategy. The statements contained herein are based on our current views and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Past performance may or may not be sustained in future. Neither HDFC AMC and HDFC Mutual Fund (the Fund) nor any person connected with them, accepts any liability arising from the use of this document. The recipient(s) before acting on any information herein should make his/her/their own investigation and seek appropriate professional advice and shall alone be fully responsible / liable for any decision taken on the basis of information contained herein.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.